Author

Leon Cheng

Leon Cheng is a Partner for YCP based in the US office and Head of our Mobility Practice.

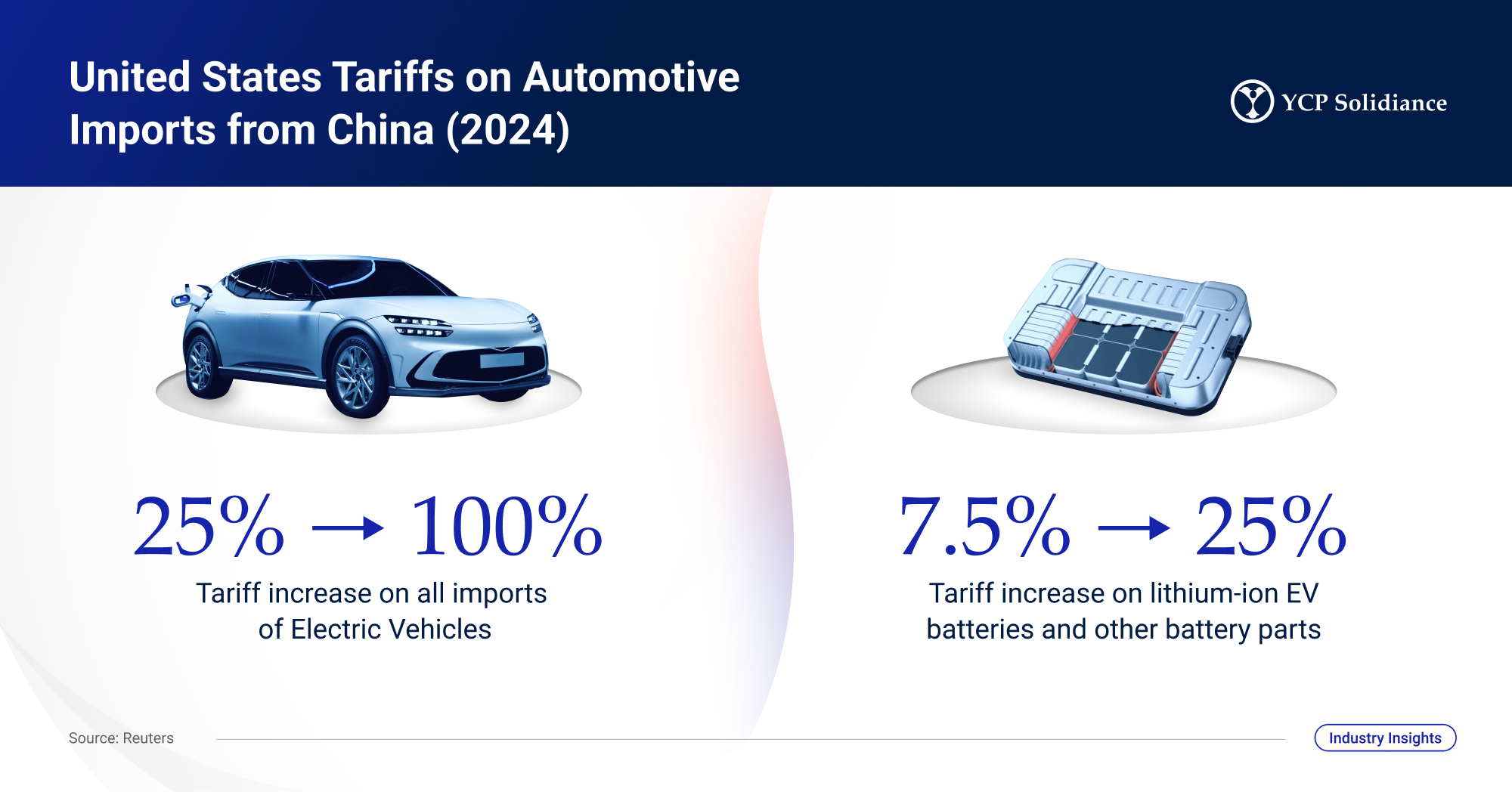

In light of recent geopolitical and economic developments, the U.S. government has announced significant tariff increases on electric vehicles (EVs) imported from China. The Biden administration is set to quadruple the current tariffs of 25% to 100%. This move aims to protect domestic auto workers and industries from the competitive pressures of subsidized Chinese EVs. However, this decision introduces new complexities for the global automotive supply chain, prompting companies to explore diversification strategies beyond China to mitigate risks and ensure resilience.

The heightened tariffs are part of a broader strategy to address trade imbalances and reduce dependency on Chinese manufacturing. The U.S. government's focus is on bolstering domestic production capabilities and fostering alternative supply chains in regions like Mexico, Vietnam, and Thailand. This shift is driven by several factors, including regulatory pressures, labor cost dynamics, supply chain resilience, and geopolitical stability

We asked YCP Solidiance Partner Leon Cheng, who works in both our North American and Asia-Pacific offices, for insight into the potential impacts diversifying automotive supply chains in China will have on the industry’s global landscape. With over 12 years of enriching experience in crafting robust strategies for automotive and mobility players, including PMO initiatives with OEM clients, the launch of new EV models, and the development of go-to-market approaches in the Asian automotive aftermarket, he shared insight into the nuanced dynamics of this development, such as growth drivers, market barriers, and how players can better adapt in the coming years.

Given China's significant role in automotive within Asia and other regions, what impact/s will diversifying supply chains in China have on the global automotive industry? How will this affect automotive players moving forward?

Such a development will undoubtedly impact the automotive industry, and it will be felt on both a macro and micro level within Asia and worldwide.

From a macro perspective, diversifying from major economies like China introduces heightened operational complexities and associated cost escalations due to tariffs and shifting trade policies. For instance, when the United States (US) imposed tariffs on Chinese goods, it affected various industries, including automotive. Thus, increasing the cost of imported automotive components could lead to higher prices for consumers.

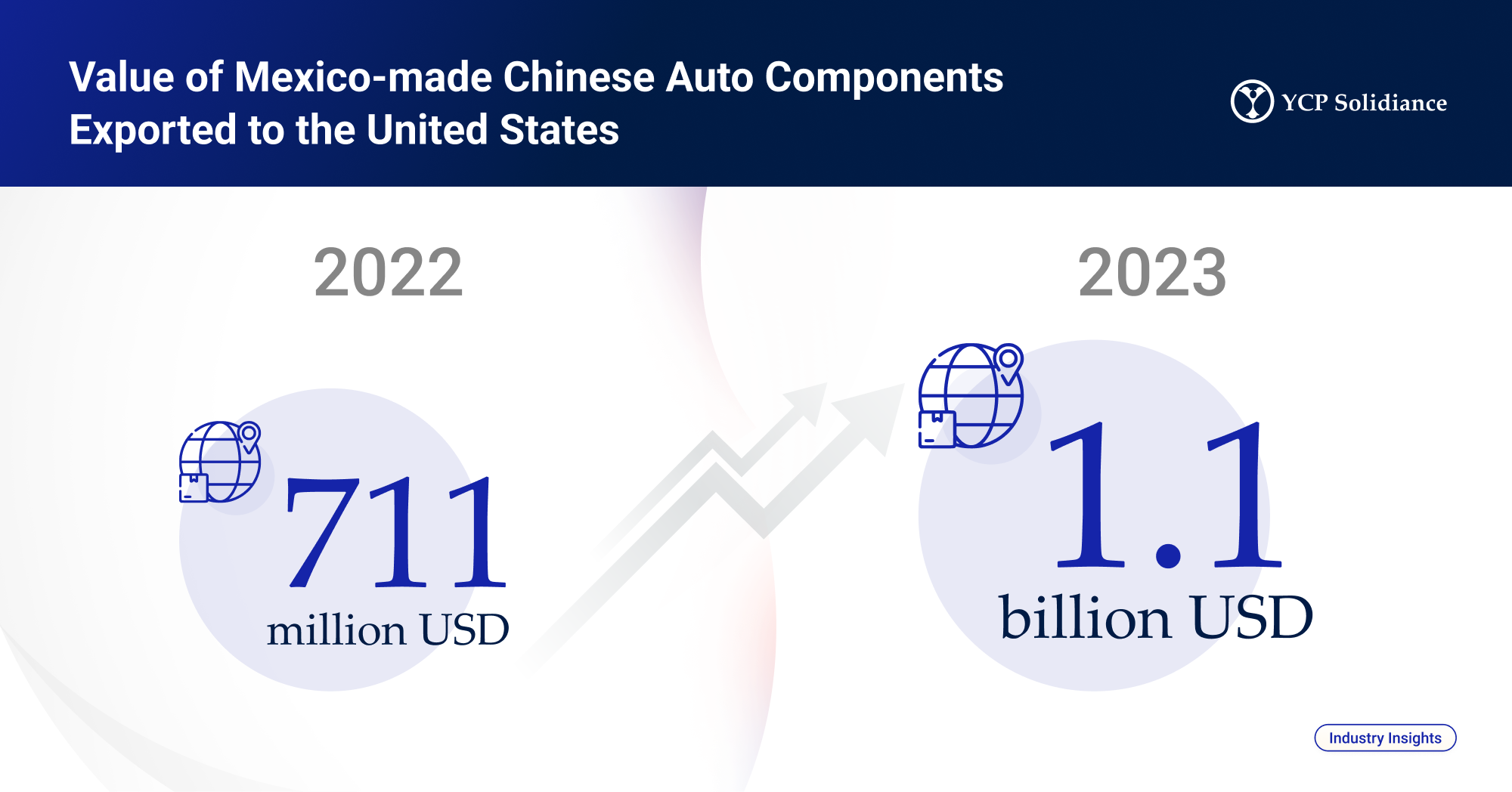

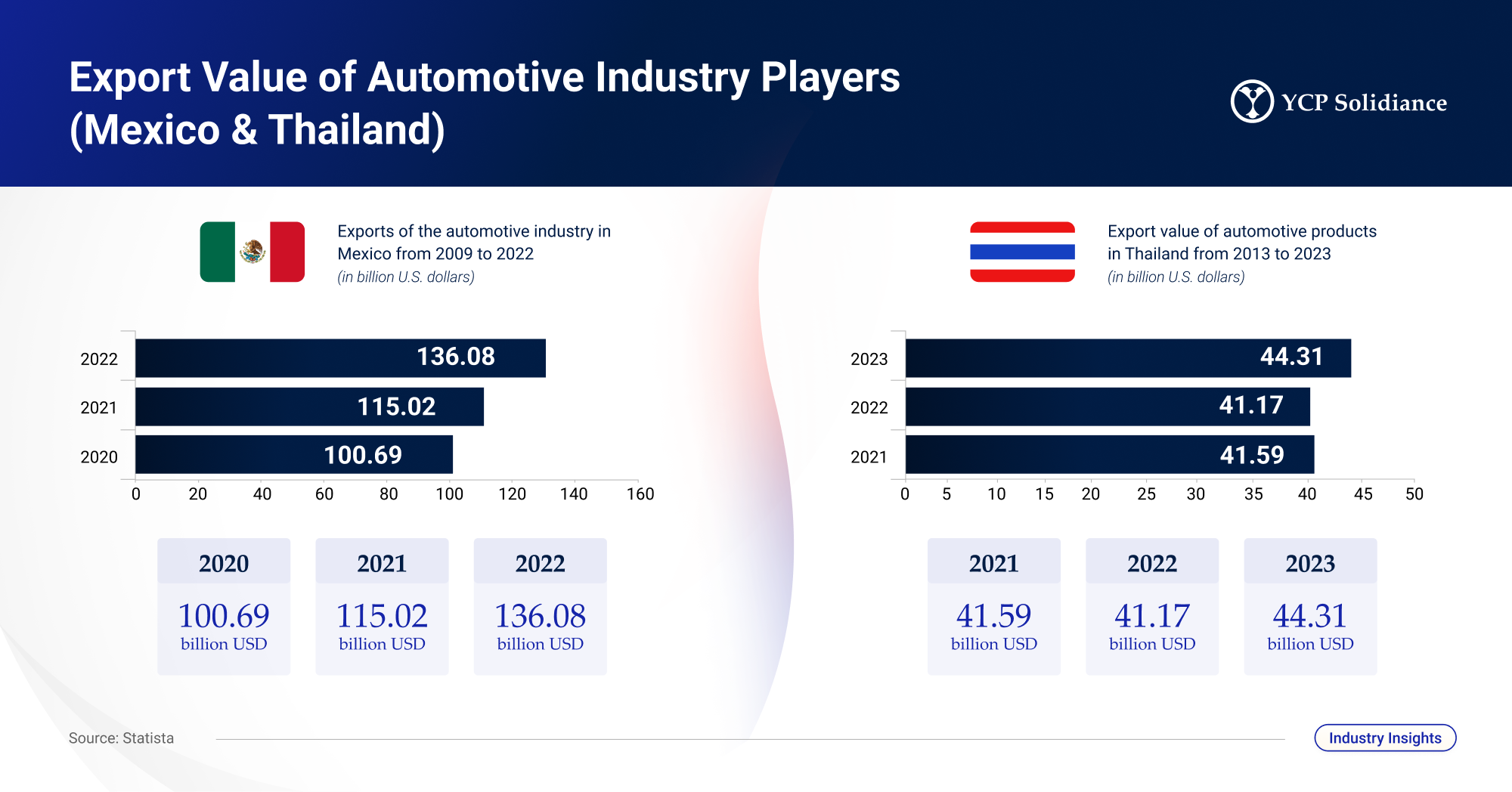

In response, we are already witnessing how automotive players are strategically pivoting towards diversifying supply chains to mitigate risks related to geopolitical tensions and supply chain vulnerabilities. Many technology and automotive companies are reducing dependency on China by pivoting towards domestic manufacturing and emerging markets such as Mexico, Vietnam, and Thailand to safeguard against trade wars and sanctions. These strategies, such as relocating supply chain operations to countries like Mexico due to existing free trade zone (FTZ) agreements with Canada and the US, or even Vietnam and Thailand—which are reasonable options due to proximity—offer promising opportunities for the industry.

Meanwhile, micro-level impacts will be felt primarily in supplier relationship reconfigurations and local market investments.

As part of diversifying supply chains outside of China, automotive OEMs and Tier 1/2 suppliers are taking steps to establish new supplier networks in alternate regions, which requires navigating regulatory changes and logistical complexities. For instance, automakers moving their supply chains to Mexico must deal with new regulatory environments, including unfamiliar or different labor laws and trade agreements. To bolster efforts, companies are investing in emerging markets to capitalize on lower costs and to be closer to new customer bases. For instance, EV manufacturers are establishing production facilities in countries like Thailand, which have favorable policies toward EVs, including government subsidies and infrastructure development.

Overall, it is clear that diversifying from China [in automotive] will alter current market dynamics for global players, fundamentally changing how involved players strategize and do business. Should other industries also diversify supply chains in China, similar implications will be felt as players attempt to replicate and deploy similar strategies in automotive.

We previously discussed how automotive supply chains are relocating to Mexico, Vietnam, and Thailand and the primary factors (FTZs and proximity) in choosing these countries as alternatives to China. Are there other factors you would like to highlight?

As automotive players continue to relocate supply chains and explore alternatives beyond China, several factors will play a key role in driving or impeding industry growth, including:

Regulatory Frameworks: Countries offering favorable policies, such as tax incentives and subsidies, attract automotive supply chain investments. An appropriate example would be how Vietnam offers various incentives for foreign investors, including reduced corporate tax rates and import duty exemptions, making it an attractive destination for automotive companies.

Labor Cost Efficiency: The automotive industry is sensitive to shifts in labor costs, which can vary significantly between countries. Rising wages in China have led companies like Apple to consider moving parts of their production to lower-cost countries such as Vietnam and India. In the automotive sector, this trend is exemplified by companies diversifying their manufacturing bases to countries like Mexico, where labor costs are more competitive than in China.

Supply Chain Robustness: The COVID-19 pandemic underscored the importance of having resilient supply chains that can withstand global shocks. Companies increasingly seek to diversify their supply bases to avoid the kind of disruptions experienced when China, a major international manufacturing hub, was initially hit by the pandemic. The shift towards countries like Vietnam and Thailand is partly motivated by the desire to create more robust supply networks less vulnerable to single points of failure.

Technological Advancements: Countries with advanced manufacturing technologies and robust infrastructure can attract automotive supply chains. For instance, Thailand's Eastern Economic Corridor (EEC) initiative aims to develop advanced technologies in the automotive sector, offering incentives and state-of-the-art facilities for EV production. This makes Thailand an attractive destination for automotive companies looking to innovate and scale up their EV capabilities.

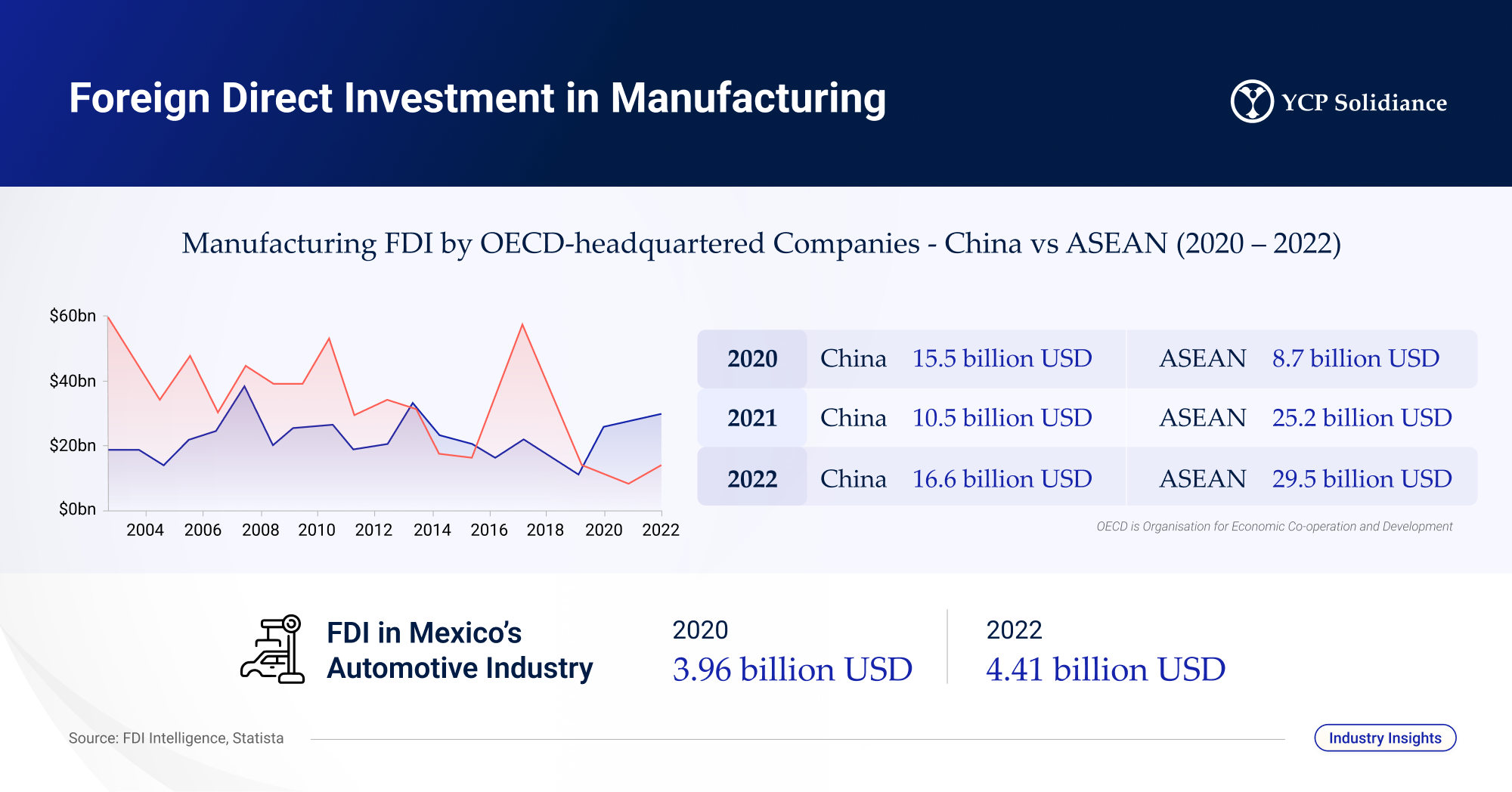

Geopolitical Stability: Companies seek to minimize risks associated with geopolitical instability and unpredictable policy environments. Mexico, for instance, offers a relatively stable political and economic environment compared to other Latin American countries experiencing tensions or conflicts. This stability, coupled with a favorable policy environment for business and foreign investments, makes Mexico an attractive hub for automotive supply chains.

While players should seek to leverage these market drivers and translate them into growth opportunities, becoming familiar with the emerging challenges of diversifying automotive supply chains in China is still important. Key challenges involve managing intricate supply networks and cultivating local infrastructure and talent. Original equipment manufacturers (OEMs) require close proximity to their facilities, resulting in a close-knit and intricate supply chain involving all the tier 1 and tier 2 suppliers and other suppliers in the chain. For instance, shifting production to a new country will be a lengthy and complex process. Players must adequately build the necessary facilities and infrastructure to support operations, while also developing or transferring technical know-how and skills to the workforce.

Despite the incentives accessible to automotive players outside of China, these challenges can significantly hinder the industry's success. New and old players alike should familiarize themselves with these drivers and growth barriers, as doing so can equip involved parties with the necessary knowledge to successfully navigate diversifying supply chains from China.

In your expert opinion, have players’ efforts to diversify automotive supply chains in China been effective? If not, how can players better adapt?

To properly determine the success of such efforts, the fundamental focus of this question should center on the origins of players diversifying from China. Are the diversification efforts really successful, especially if the companies migrating their operations are still Chinese players, either privately owned or backed by the Chinese government?

Ultimately, it may be difficult to accurately determine the number of Chinese players who migrated operations to other countries. Regardless, policymakers and private companies can deploy several strategies to bolster supply chain diversification.

From a policymaker’s perspective, on top of tariff and trade restrictions, it is essential to stimulate and incentivize domestic manufacturing through subsidies, tax breaks, and grants, which will help encourage automotive players to invest in local manufacturing capabilities. Further investments should also be dedicated to enhancing research and development of infrastructure and innovation ecosystems, as it can make domestic locations more attractive for high-tech automotive components manufacturing, such as EV batteries and semiconductors. In addition to these investments, private sector players should leverage strengthened trade alliances, where governments should form or enhance trade agreements with alternative manufacturing hubs that can facilitate easier market access and incentivize companies to diversify their supply chains away from over-reliance on a single country like China.

Meanwhile, automotive players' primary goal should be to create global resilient and robust supply chains within the industry. This can be achieved by distributing investment across different aspects of the value chain, such as:

Implementing Supplier Base Diversification: Instead of relying on suppliers from a single country or region, automotive companies can mitigate risks by sourcing materials and components from various countries. For example: Increasing the number of countries from which critical components are sourced to avoid bottlenecks when one region faces disruptions.

Adopting Innovative Materials & Technologies: Innovation in materials science and manufacturing technologies can reduce dependency on specific countries for rare or critical materials (e.g., alternative battery chemistries less reliant on rare earth elements predominantly sourced from China.)

Enhancing Supply Chain Transparency: Companies could invest in technologies like blockchain and IoT to enhance transparency and agility in their supply chains, allowing for quicker adaptation to disruptions.

Strategic Stockpiling: Building strategic reserves of critical components can help buffer against short-term disruptions in the supply chain.

Proactively Engage Chinese Suppliers: Automotive companies can proactively diversify their supply chains by assisting their current Chinese suppliers in establishing a supply chain in overseas markets either through a joint venture or licensing manufacturing. This will help them have better control over their supply chains while benefiting from the advanced manufacturing capabilities of the Chinese suppliers.

Though these strategies can work and unlock beneficial growth opportunities, I do not think any policy or strategy can be perfect, especially in areas as complex as the automotive supply chains. Diversifying from China, particularly for the automotive industry, is a nuanced issue that cannot be approached with a one-size-fits-all strategy. The complexity and interconnectedness of global supply chains, especially those entrenched in the automotive sector, make immediate and perfect solutions improbable. Given this context, the effectiveness of diversification strategies needs to be assessed continuously, accounting for the dynamic nature of global trade, technological advancements, and geopolitical shifts.

While diversifying from China presents considerable challenges, especially in the automotive industry, it opens avenues for reflection on global supply chain dynamics. For sustainable growth and to build a more resilient supply chain ecosystem, companies should focus on diversifying their supplier networks, investing in supply chain visibility, and leveraging cutting-edge materials and technologies. The effectiveness of these efforts will depend on continuous evaluation and the willingness to adapt strategies in response to evolving global trends and challenges.

How can YCP help stakeholders (investors, private players, etc.) in the global automotive industry?

Strategic Planning and Market Analysis – YCP utilizes its deep expertise in market analysis and strategic planning to assist clients through the intricacies of supply chain adjustments. This involves a comprehensive examination of factors such as labor costs, regulatory landscapes, and logistics.

For a client considering a partial production shift to alternative regions like SEA, India, and Mexico, YCP could conduct a detailed feasibility study. This study would delve into the target region's labor cost structures, evaluate the regulatory environment to ensure compliance, and assess logistical frameworks to guarantee efficient production and distribution. The objective would be to offer precise, actionable insights to facilitate the client's decision-making process.

M&A Support - Carving Out China Operations – YCP provides specialized M&A support to companies looking to restructure their operations through divestitures, specifically carving out segments of their business related to China.

For MNC automotive players aiming to divest their Chinese entities/assets, YCP would offer end-to-end advisory services. This includes evaluating the division's financial performance and strategic fit, preparing the business for sale, identifying potential buyers, managing the negotiation process, and post-divest implementation support such as shared services transition. The goal is to ensure a smooth transition that maximizes value for the client while aligning with their global strategy.

Supply Chain Consulting - Assessing and Selecting New Suppliers – In the realm of supply chain consulting, YCP excels in evaluating and establishing a reliable and resilient new supplier base in alternative markets. This service is critical for companies looking to diversify their supplier base away from China and mitigate risks associated with geopolitical tensions and supply chain disruptions.

For a client seeking to broaden its supply chain to include suppliers in countries like Vietnam and Thailand, YCP would conduct a comprehensive assessment of potential suppliers and even manage the new suppliers afterward. This process involves analyzing the suppliers' capabilities, financial stability, compliance with international standards, and the ability to scale operations. YCP's insights would enable the client to make informed decisions, ensuring a resilient and diversified supply chain. Furthermore, YCP’s supply chain division can optimize and manage the newly established supply chain via innovative AI solutions and digital platforms.

Leon Cheng is a Partner at YCP Solidiance with a dual base in the North American and Asia-Pacific offices, leading the firm’s global mobility practice. His 12 years of consulting within the automotive and mobility sector encompass strategy, M&A, process improvement, and supply chain optimization. Leon has directed over 100 projects, driving growth for automotive OEMs, suppliers, and service providers throughout the mobility value chain. He holds a Bachelor’s degree in management from the University of Finance and Economics of Anhui and an MBA from the University of Science and Technology of China.

Special thanks to the Auto Care Association for their contribution to this report.